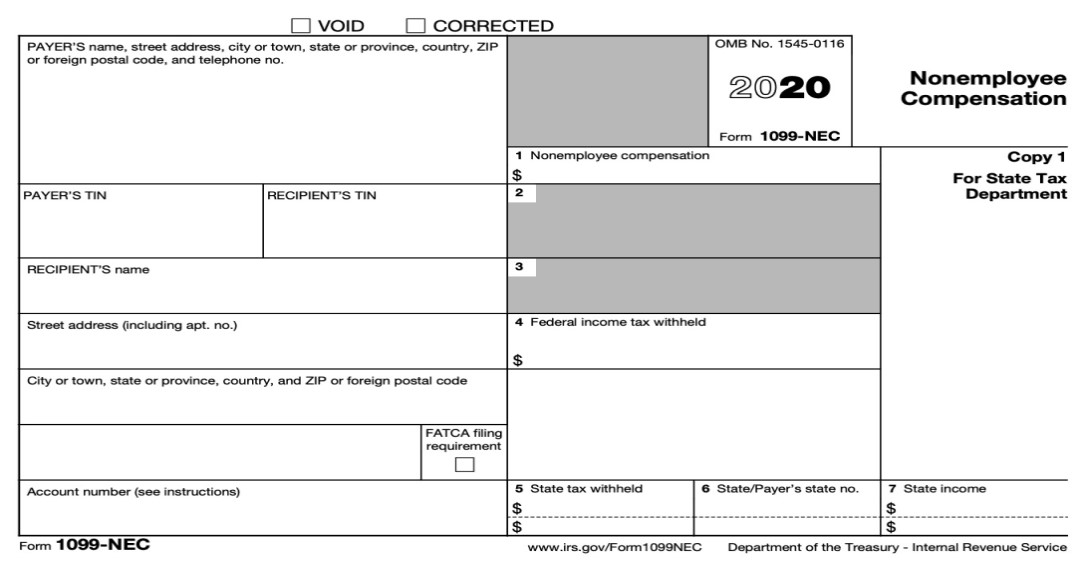

The IRS has introduced a new Form the 1099-NEC. The NEC is short for non employee compensation. This is the new form for reporting independent contractor income. The 1099-Misc will not be used to report income for individuals who’re self-employed in 2020.

What is a 1099-NEC?

The 1099-NEC is a new form created to report non-employee compensation.In previous years all independent contractors would receive a 1099-MISC form with the amount paid to you being reported in the box 7. The requirements to file a 1099-NEC are still the same as a 1099-Misc.

A 1099-NEC needs to be filed if your business paid any contractor more than $600 in a single tax year. You must also file Form 1099-NEC for each person from whom you have withheld any federal income tax (report in box 4) under the backup withholding rules regardless of the amount of the payment. Payments to a corporation including a limited liability company (LLC) that elected to be treated as a C or S corporation will not be required to file 1099-NEC. The exemption from reporting payments made to corporations does not apply to payments for legal services. Therefore, you must report attorneys’ fees (in box 1 of Form 1099-NEC). The entity type should be reported to you on a W-9 form.

Responsibilities for filing 1099-NEC?

It’s your company’s responsibility to file the Form 1099-NEC with the IRS and send a copy to the independent contractor by January 31. The due date is similar to the W-2’s. There are two copies that need to be filled out. Copy A is sent to the IRS while Copy B needs to be sent to the contractor. You can either e-file or send through mail.

If you missed the January 31st deadline, you will end up paying a penalty depending on how late the filing is. These penalties are:

$50 if you file within 30 days

$100 if you file more than 30 days late, but before August 1

$260 if you file on or after August 1

If you are unable to file on time, you can request an extension by submitting Form 8809 to the IRS. However, you will still need to supply the 1099-NEC forms to any contractors by January 31.If you need assistance completing your 1099 NEC. Please reach out to International Accounting & Tax Consultants (IATC Inc) at www.iatcpro.com.

The President signed the “Consolidated Appropriations Act, 2021 into law. This law provided $284B dollars to be used for the second round of the Paycheck Protection Program. The application deadline for businesses wanting to receive a PPP2 loan is March 31, 2021. Due to the high demand expected, businesses should apply as early as possible. It is very likely the funds will be exhausted before the actual March deadline.

If your company received the first round of funding you are not automatically excluded from the second round of funding.

The new PPP2 loan requirements are a little different from the first round:

Your company must have less than 300 employees.

Must have been in operation before February 15, 2020.

Cannot be a publicly traded company.

Can’t be a business primarily engaged in political advocacy or lobbying.

Your company can not have significant ownership by Residents of China.

You must now be able to show at least a 25% reduction in gross revenue in any quarter of 2020 compared to the same quarter in 2019. If your business was new and didn’t exist the entire year of 2019. Use the quarters you were in business before February 2020.

Your business must have used the previous PPP loan or have a plan in place to use all of their original PPP loan for approved expenses.

PPP2 Forgiveness

The maximum amount of each loan is maxed at $2 million. Each entity can only have one PPP2 loan. The PPP2 loan forgiveness rules are similar to the PP1 rules. Payroll costs should account for at least 60% of the PPP2 loan amount spent and any remaining should be spent on other approved costs, all within the covered forgiveness period. The forgiveness period starts when you receive your PPP2 money in your bank account. Your company will either have an 8-week or a 24-week covered period of forgiveness. The approved Payroll costs includes an employee salary and benefits like vision and dental benefits. The “other” approved expenses would be the rent, mortgage interest, and utilities. Payments for software, cloud computing, HR systems, and accounting needs.

The PPP2 program included other additional expenses that are allowed to be covered. Any repair costs associated with looting or vandalism during 2020 disturbances when the cost of repairs were not covered by any insurance. Any payments made for essential goods for periods before the PPP2 loan was received. Payments for perishable items can also be made either before or after the PPP2 loan is received. Any PPE equipment or facility modification expenditures spent by your business to comply with COVID-19 federal health and safety guidelines. This would include items like face masks, drive-through windows, thermometers, and even HVAC improvements from March 1, 2020 throughout the year.

IATC Inc encourages businesses that qualify to apply as soon as possible for the PPP2 loan. If you need detailed information please feel free to contact us at www.iatcpro.com

The 2020 year is coming to a close and for most people their focus is the holidays. Taxes season is also upon us. There are a few things people can do to minimize their tax burden before the year is completely Over.

Give to a Charity

Donating to a charity is a great way to reduce taxes if you itemize. You can support a great cause and help yourself all at the same time. To take this deduction your charity donations need to be paid to a 501(c)(3) organization. Your ability to deduct cash donations is limited to 60% of adjusted gross income. For property donations, the deduction is limited to either 30% of your adjusted gross income when using fair market value of the property or 50% of your adjusted gross income if you’re using a cost basis to determine the amount of the deduction. The CARES Act created a new $300 dollar cash donation deduction for individuals that take the standard deduction in 2020.

IATC Inc currently partners with a local nonprofit organization www.hyncharity.org. We donate a portion of our profits to help this 501(c)(3). Helping Your Neighbor Charity promotes long-term self-sufficiency and empower at risk community members through safe green housing, financial literacy, and career development.

Maximize IRA, SEP, and Roth Contributions

One easy way to reduce your taxable income before the year is over is to max out allowable 401(k) contributions. “Of course, this will provide a boost for your retirement, but as a bonus, qualified contributions will lower your taxable income for the year,” For 401(k), 403(b), and many 457 plans, as well as the federal government’s Thrift Savings Plan, the annual contribution limit is $19,500, up from $19,000.

For self employed people your business can contribute to an SEP

The amount of contributions made to each employee’s SEP-IRA each year cannot exceed the lesser of:

25% of compensation, or

$57,000 for 2020 ($56,000 for 2019 and subject to annual cost-of-living adjustments for later years).

These limits apply to contributions you make for your employees to all defined contribution plans, which includes SEPs. Compensation up to $285,000 in 2020.

Bonus Tip. Once you contribute the maximum allowable amount to your SEP-IRA of $57,000 from the business. You are allowed to also make regular, annual IRA contributions to your Roth IRA and Regular IRA but your total contributions still cannot exceed $6,000 for 2020.

Make Estimated Tax Payments

Our tax system is a pay as you go system so taxes are supposed to be paid as you earn or receive income during the year, either through withholding or estimated tax payments. If the amount of income tax withheld from your salary or pension is not enough, or if you receive income such as interest, dividends, alimony, self-employment income, capital gains, prizes and awards, you may have to make estimated tax payments. This is a common issue with self-employed individuals.

If you don’t pay enough tax through withholding and estimated tax payments, you may be charged a penalty for underpayment of estimated taxes. You may also be charged a penalty if your estimated tax payments are late, even if you are due a refund when you file your tax return. To avoid this penalty you need to owe less than $1,000 in tax after subtracting your withholdings and credits. You need to have paid at least 90% of the tax due for the current year, or 100% of the taxes owed on the prior year return, whichever amount is smaller.

Update Information with Past Employers and Banks

It’s normal for people to move and get new jobs throughout the year. Before the year end you should check with your prior employers and confirm they have your correct mailing and email addresses. I would do this as early as November. Employers must file Form W-2 and other wage statements by January 31, 2021, to avoid penalties and help the IRS prevent fraud. In actual practice most employers are sending the W-2s, and 1099’s out via mail and electronically the first two weeks in January.To make sure your forms make it to you on time, and not someone else. I recommend people confirm with each employer, bank, contractor, or other payers to ensure they have your current mailing address or email address.

Defer Additional Bonuses

End of the year bonuses are normally accounted for when I do tax planning with my clients. Sometimes you just have a great year and the bonus amounts push you into an even higher tax bracket. Companies that pay bonuses are familiar with employees requesting that their bonuses not be paid out until January of the new year. This will help you defer the taxes on that income until the next tax year. A useful strategy for individuals who might see their income decline in the upcoming year.

If you live or work outside the United States did you know you can actually exclude almost $100,000 of your income tax free.

The Foreign Earned Income Exclusion is a one of the largest tax benefits available to you as US resident living or working abroad. This is something an expat would love almost as much as traveling abroad.

Expat is a short way of saying expatriate. An expatriate is defined as a person residing in a country other than their native country.

If you take this exclusion your first $97,600 earned overseas is going to be exempt from income tax.

Before you pack up the family and hop on a plane thinking you are about to just live tax free overseas. Not everyone can actually qualify for this exclusion.

In order to qualify for the Foreign Earned Income Exclusion, you must meet one of two test.

1) The Bona Fide Residence Test.

2) The Physical Presence Test.

Bona Fide Residence Test

You meet the bona fide residence test if you are a bona fide resident of a foreign country or countries for an uninterrupted period that includes an entire tax year. You can use the bona fide residence test to qualify for the exclusions and the deduction only if you are either:

A U.S. citizen, or

A U.S. resident alien who is a citizen or national of a country with which the United States has an income tax treaty in effect.

You do not automatically acquire bona fide resident status just by living in a foreign country or countries for 1 year. If you go to a foreign country to do work for a particular job for a specified period of time, you will normally not be considered a bona fide resident of that country even though you have worked there for 1 tax year or longer. The length of your stay and the nature of your job are only some of the factors that goes into determining whether you can meet the bona fide residence test.

Bona fide residence. To meet the bona fide residence test, you must have established a bona fide residence in a foreign country.

Your bona fide residence is not necessarily the same as your domicile. Your domicile is your permanent home, the place to which you always return or you intend to return.

You could have your domicile in Nashville, Tennessee and a bona fide residence in Sydney, Australia. Nashville will be a bona fide residence, if you intend to return eventually to Tennessee.

The fact that you visit Australia does not automatically make Australia your bona fide residence. If you go there as a tourist, or on a short business trip, and return to the United States, you have not established a bona fide residence in Australia. If you go to Australia to work for an indefinite or extended period and you set up permanent quarters there for yourself and your family, there is a good chance you can claim you have established a bona fide residence in a foreign country, even if you intend to return to the United States someday in the future.

Now in real life it can be more difficult to decide whether you have actually established a bona fide residence. If you have any doubt or concerns feel free to reach out to IATC Inc for help.

Your bona fide residence will be determined according to each individual case, taking into account three main factors such as your

Intention,

Why you are visiting and

The nature and length of your stay abroad.

A treaty that prevents you from becoming a bona fide resident of a foreign country is determined based on each individual treaty. All provisions of a treaty you could be subject including specific provisions relating to residence or privileges and immunities should be reviewed as well.

To meet the bona fide residence test, you must reside in a foreign country or countries uninterrupted for an entire tax year. An entire tax year is from January 1 through December 31 for taxpayers on a calendar year basis.

An entire year without seeing family or friends might be too difficult a task for some. You are allowed to leave the country for a brief or temporary trip back to the United States or somewhere else for vacation or business. And still be a bona fide residence in a foreign country, To keep your status as a bona fide resident of a foreign country, you must have a clear intention of returning from the trips, without unreasonable delay, to your foreign residence or to a new bona fide residence in another foreign country.

Once you have established bona fide residency in a foreign country for an uninterrupted period that includes an entire tax year, you are a bona fide resident of that country for the period starting with the date you actually began the residence and ending with the date you abandon the foreign residence. Your period of bona fide residence can include an entire tax year plus parts of 2 other tax years.

If you are assigned from one foreign location to another, you may or may not have a break in foreign residence between your assignments, depending on the circumstances.

The second physical presence test can be more confusing when applying to a person tax return. To be qualified for the exclusion based on your physical presence means you can leave the United States for business and can not return for more than 35 days throughout the past twelve months. This test is also not based on a calendar year. You can qualify by using any twelve month period of time.

One thing to keep in mind is with the 35 day limit. The days do not have to run straight in a row. You can become ineligible to take the exclusion if you have taken multiple trips back to the US that exceeds 35 days in the US during a 12 month period.

The Deductions

If a person meets the foreign income exclusion they are allowed to deduct up to $97,600 of their foreign earned income from their US taxes. If you are married filing jointly, you would be able to deduct up to double that from your US taxes. This amount is also indexed for inflation and increases each year.

The Foreign Earned Income Exclusion relies solely on foreign income for calculation purposes and the income must be earned. Foreign income from passive sources such as dividends, interest, retirement income, and rental income are not included since those income sources are not considered “earned” income.

Additional Complexities

There are some additional complexities to the Foreign Earned Income Exclusion, so it is almost always advisable to consult with a tax expert about your specific situation at www.iatcpro.com

Self employed individuals having to still pay their Self-Employment tax to the US. After paying your self employment taxes you can exclude your earnings.

Not all US expats are able to take advantage of the foreign earned income exclusion. If you are a US Government Employee and are paid by the US government then you will not be able to use the Foreign Earned Income Exclusion to minimize your US expat taxes. This includes individuals in the Armed Forces Exchange, Commissioned and non-commissioned Officers’ messes, Armed Forces motion pictures services and employees of kindergartens on Armed Forces installations.

Tax credits.

if you claim either of the foreign income exclusion, You can’t take the additional child tax credit or earned income credit.

Additional Income: If you decided to rent your property while you were living abroad. Your rental income is still going to be reported, along with your usual expenses.

Need to File State Returns: Living or working abroad does not eliminate your need to file a state tax return with some states. Certain taxpayers must maintain a state of domicile in the United States, and there will be tax obligations to that state.

Retirement: If you are still making contributions to your retirement accounts, even if it’s your SEP, IRA or ROTH IRA they are all subject to certain limits based on your gross income. If you plan to claim your IRA deduction, special rules apply.

Foreign Housing Exclusion or Deduction: In addition to the foreign earned income exclusion, you can also claim an exclusion or a deduction from gross income for your housing amount if your tax home is in a foreign country, you have self employment income, and you qualify under either the bona fide residence test or the physical presence test.

Even though you are ineligible your spouse can claim this exclusion be if they are not government and work overseas. If you are having a hard time determining your eligibility for the foreign earned income exclusion schedule an appointment at www.iatcpro.com.

Every year after the extension due date new clients contact me ready to file their tax return. This is the time we find out extensions were not actually file, and now they have multiple penalties and interest to pay. I get them updated and write a letter to abate penalties.

The IRS isn’t in the business of letting people keep money. Penalty abatement is kind of easy the first time around for most clients. Some people don’t even feel it worth asking for penalty abatement/relief because everything involving the IRS is too complicated and time consuming. This is the part where I push up my glasses and tighten the tie getting ready to handle the hard part on their behalf.

I think taxpayers need to understand why the IRS actually uses penalties. Penalties are supposed to be a deterrent for people who fail to follow the rules and are out of compliance with the US tax code. They are a great way to bring in revenue for a under funded government branch so expect to see them applied whenever possible. The IRS apply millions of penalties to tax payers every year bringing in billions of easy money. Life happens and there are additional options to get penalties removed, or abated, for individuals ans businesses that qualify.

The most common used IRS penalties is the failure to file and failure to pay.

The IRS has over 130 different penalties the can assess. in the Internal Revenue Code, but two penalties make up 75% of all penalties assessed by the Internal Revenue Service.

Failure to pay penalty equals 60% of all penalties.

Failure to file penalty equals approximately 15% of all penalties.

The tax penalties can be disputed by providing an exception when filing your tax return.

Penalties will be removed by the Internal Revenue Service for a few reasons. We normally end up requesting penalty abatement for a statutory exception or reasonable cause.

Statutory exception- Are specific authoritative exclusions to the penalties. Statutory exceptions are rare, but rather easy to make a case for. A statutory exception would be a presidential declared disaster relief.

IRS Fault: If you can prove an error was the result of reliance on IRS advice. We always caution against following an agents advice. We default to the US Tax code and use that. To use the IRS error for a penalty relief is difficult and rarely successful. You need to have documented erroneous advice from the IRS that you reasonably relied on. The IRS doesn’t put tax advice in writing in majority of cases. You can also file penalty abatement based on erroneous verbal advice. Being able to successfully use either argument is not common.

Reasonable cause: providing a valid reason that you couldn’t comply based on your facts and circumstances. This argument normally includes chronic health problems and reliance on a bad tax professional or tax software. Those types of problems can be used under reasonable cause.

To successfully apply for an abatement using a reasonable cause argument for late filing and payment has its own requirements. You must demonstrate that you genuinely tried to comply. Your actions should demonstrate a sense of care. You need to show that your noncompliance was not due to your willful neglect.

IRS agents are also citizens and taxpayers just like you. To successfully prove a reasonable cause, you’ll need to make sure that the IRS knows all of the facts around the circumstances. It can seem unnecessary, but not all situations are the same. Leaving out facts that can clarify your position could result in you receiving a denial letter. If the denial letter fails to address facts crucial to your argument presented earlier. The option to request an appeal of the determination should be explored.

The IRS can provide administrative relief from a penalty under certain conditions. The most widely used relief is the first-time penalty abatement (FTA). FTA can be used to abate your failure to file, failure to pay, and other penalties for a single tax period. You do need to have a good history of filing your returns. You can use first time penalty abatement for your business tax penalties as well. FTA is the easiest of all penalty relief options to get approved. You just have to ask for it. If you need help with the IRS you should contact iIATC Inc for tax resolution services.

It wasn’t but a few years back when crypto currency started making mainstream news. IRS had not provided guidance on how to tax the currency. Crypto users were positive they wouldn’t have to pay taxes, because the government wouldn’t have the information needed to track them. Fast forward to 2019 and now the IRS is sending over 10,000 letters to crypto currency holders informing them of their tax duties. The IRS obtained the names of the taxpayers through summons given to the crypto exchanges.

The IRS Large Business and International division (LB&I) had previously announced the approval of five additional compliance campaigns. LB&I’s goal is to improve return selection, identify issues representing a risk of non-compliance, and make the greatest use of limited resources. In plain english their job is to find tax returns with a high chance of errors and collect money and interest from that taxpayer. As a U.S. person you are subject to tax on worldwide income from whatever source derived, including transactions involving virtual currency.

The IRS has a focus on this area with real intentions on curbing noncompliance by taxpayers. The IRS letters are also conveying different messages to taxpayers. The letters were aiming to educate some taxpayers, while others are receiving letters about audits or criminal investigations being pursued. Professionals at IATC Inc always advocate staying in compliance with the tax code to avoid penalties and fines. Crypto traders should contact us for help with any letters they receive.

Recent Comments