by Donya Curry | Jan 12, 2021 | Bookkeeping, Business, Individuals, Non Profits

The IRS has introduced a new Form the 1099-NEC. The NEC is short for non employee compensation. This is the new form for reporting independent contractor income. The 1099-Misc will not be used to report income for individuals who’re self-employed in 2020.

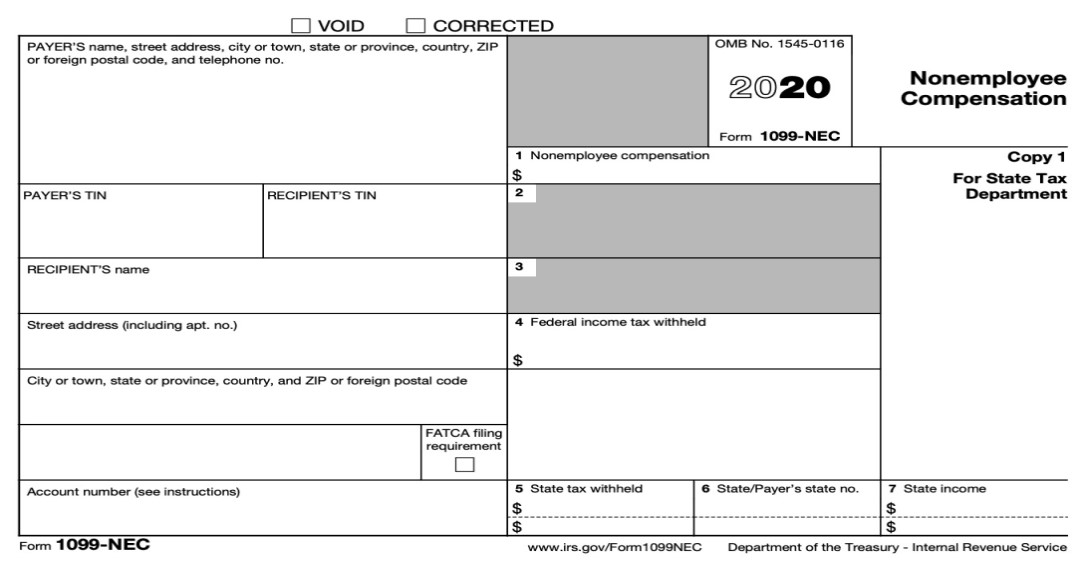

What is a 1099-NEC?

The 1099-NEC is a new form created to report non-employee compensation.In previous years all independent contractors would receive a 1099-MISC form with the amount paid to you being reported in the box 7. The requirements to file a 1099-NEC are still the same as a 1099-Misc.

A 1099-NEC needs to be filed if your business paid any contractor more than $600 in a single tax year. You must also file Form 1099-NEC for each person from whom you have withheld any federal income tax (report in box 4) under the backup withholding rules regardless of the amount of the payment. Payments to a corporation including a limited liability company (LLC) that elected to be treated as a C or S corporation will not be required to file 1099-NEC. The exemption from reporting payments made to corporations does not apply to payments for legal services. Therefore, you must report attorneys’ fees (in box 1 of Form 1099-NEC). The entity type should be reported to you on a W-9 form.

Responsibilities for filing 1099-NEC?

It’s your company’s responsibility to file the Form 1099-NEC with the IRS and send a copy to the independent contractor by January 31. The due date is similar to the W-2’s. There are two copies that need to be filled out. Copy A is sent to the IRS while Copy B needs to be sent to the contractor. You can either e-file or send through mail.

If you missed the January 31st deadline, you will end up paying a penalty depending on how late the filing is. These penalties are:

$50 if you file within 30 days

$100 if you file more than 30 days late, but before August 1

$260 if you file on or after August 1

If you are unable to file on time, you can request an extension by submitting Form 8809 to the IRS. However, you will still need to supply the 1099-NEC forms to any contractors by January 31.If you need assistance completing your 1099 NEC. Please reach out to International Accounting & Tax Consultants (IATC Inc) at www.iatcpro.com.

by Donya Curry | Jan 11, 2021 | Bookkeeping, Business, Individuals, Non Profits

The President signed the “Consolidated Appropriations Act, 2021 into law. This law provided $284B dollars to be used for the second round of the Paycheck Protection Program. The application deadline for businesses wanting to receive a PPP2 loan is March 31, 2021. Due to the high demand expected, businesses should apply as early as possible. It is very likely the funds will be exhausted before the actual March deadline.

If your company received the first round of funding you are not automatically excluded from the second round of funding.

The new PPP2 loan requirements are a little different from the first round:

Your company must have less than 300 employees.

Must have been in operation before February 15, 2020.

Cannot be a publicly traded company.

Can’t be a business primarily engaged in political advocacy or lobbying.

Your company can not have significant ownership by Residents of China.

You must now be able to show at least a 25% reduction in gross revenue in any quarter of 2020 compared to the same quarter in 2019. If your business was new and didn’t exist the entire year of 2019. Use the quarters you were in business before February 2020.

Your business must have used the previous PPP loan or have a plan in place to use all of their original PPP loan for approved expenses.

PPP2 Forgiveness

The maximum amount of each loan is maxed at $2 million. Each entity can only have one PPP2 loan. The PPP2 loan forgiveness rules are similar to the PP1 rules. Payroll costs should account for at least 60% of the PPP2 loan amount spent and any remaining should be spent on other approved costs, all within the covered forgiveness period. The forgiveness period starts when you receive your PPP2 money in your bank account. Your company will either have an 8-week or a 24-week covered period of forgiveness. The approved Payroll costs includes an employee salary and benefits like vision and dental benefits. The “other” approved expenses would be the rent, mortgage interest, and utilities. Payments for software, cloud computing, HR systems, and accounting needs.

The PPP2 program included other additional expenses that are allowed to be covered. Any repair costs associated with looting or vandalism during 2020 disturbances when the cost of repairs were not covered by any insurance. Any payments made for essential goods for periods before the PPP2 loan was received. Payments for perishable items can also be made either before or after the PPP2 loan is received. Any PPE equipment or facility modification expenditures spent by your business to comply with COVID-19 federal health and safety guidelines. This would include items like face masks, drive-through windows, thermometers, and even HVAC improvements from March 1, 2020 throughout the year.

IATC Inc encourages businesses that qualify to apply as soon as possible for the PPP2 loan. If you need detailed information please feel free to contact us at www.iatcpro.com

by Donya Curry | Apr 4, 2020 | Bookkeeping

As everyone knows the entire world is currently facing an unprecedented economic disruption due to the Coronavirus (COVID-19) outbreak. In an attempt to help businesses,The CARES Act was signed into law March 27, 2020 in the US, which provides over $370 billion dollars in funding for American small businesses and employees. Out of this came multiple avenues of funding for businesses through the SBA or Small Business Administration.

EIDL 10k Loan advance

The first relief program is the Economic Injury Disaster Loan Emergency Advance. This advance is for any small business owners in the U.S. currently experiencing a temporary loss of revenue due to the COVID-19 pandemic. The application is on the sba.gov website and if a business applies they will receive the Economic Injury Disaster Loan advance of up to $10,000. The $10,000 is supposed to be available in days time after submitting an application and there is no need to pay it back. The amounts over 10k will be the SBA loan to help a business that has lost income because of the Covid-19 pandemic.

This program is for any small business with less than 500 employees (including sole proprietorships, independent contractors and self-employed persons), private non-profit organization or 501(c)(19) veterans organizations affected by COVID-19.

You can also watch the video blog of this at https://youtu.be/CZUR8F1cPPM

Paycheck Protection Program

The Paycheck Protection Program is a loan designed to motivate small businesses to keep their workers on the payroll. Any small business with less than 500 employees this includes sole proprietorships, independent contractors and other self-employed people, private non-profit organizations or 501(c)(19) veterans organizations affected by coronavirus/COVID-19. This program right now is not for independent contractors. That is an ongoing conversation so that will be addressed on its own, since it will be its own program from everything I’m seeing.

Businesses in certain industries may have more than 500 employees if they meet the SBA’s size standards for those industries.Small businesses in the hospitality and food industry with more than one location could also be eligible if their individual locations employ less than 500 workers.

SBA will forgive these loans if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities. One important detail is at least 75% of the forgiven amount must have been used for payroll. Which makes sense if you want to get small businesses to keep people employed and on payroll. The loan forgiveness is based on maintaining or quickly rehiring your employees. When rehired you can not reduce their pay or salary you need to maintain the current salary levels. Forgiveness amount will be reduced if the full-time headcount declines, or if salaries and wages decrease. The loan has a maturity time of 2 years and an interest rate of 1% .

There were 10 million people who applied for unemployment insurance so far. This program is to help get those individuals rehired and not have to file unemployment claims. If your business fired employees after February 15th this should be used to get those people rehired quickly. If you are an employee that was laid off be sure to inform your employer about this program as well. You do need to apply at any existing SBA 7(a) lender or through any FDIC insured bank or credit union. Other regulated lenders will be available to make these loans once they are approved and enrolled in the program. Based on the current demand most major banks are having issues keeping up. The applications just opened on April 3rd, and most major banks are still not prepared. First check with the largest bank you currently have your accounts with.

You can also watch the video blog of this at https://youtu.be/3kBDptMIIAO

SBA Debt Relief

For businesses who are already in an SBA loan the SBA have relief options for them as well.

The SBA will automatically pay the principal, interest, and fees of current 7(a), 504, and microloans for a period of six months.

The SBA will also automatically pay the principal, interest, and fees of new 7(a), 504, and microloans issued prior to September 27, 2020.

For current SBA Serviced Disaster (Home and Business) Loans: If your disaster loan was in “regular servicing” status on March 1, 2020, the SBA is providing automatic deferments through December 31, 2020. The deferral of the payments does not mean the amounts are forgiven. The Interest will continue to accrue on the loan taken out from the SBA. The deferment will NOT cancel any scheduled or recurring payments on your existing loans. If you are a business that needs to defer payments, you are responsible for canceling those automatic payments. After the automatic deferment period, borrowers will be required to resume making regular principal and interest payments. Plan ahead to reestablish the recurring payments.

SBA Express Bridge Loans

Express Bridge Loan Pilot Program allows small businesses who currently have a business relationship with an SBA Express Lender to access up to $25,000 quickly. These loans can provide vital economic support to small businesses to help overcome the temporary loss of revenue they are experiencing and can be a term loan or used to bridge the gap while applying for a direct SBA Economic Injury Disaster loan. If a small business has an urgent need for cash while waiting for a decision and disbursement on an Economic Injury Disaster Loan, they may qualify for an SBA Express Disaster Bridge Loan. This loan like the Paycheck Protection Program is also taking into account what you receive from the Economic Injury Disaster Loan. The 25k you receive will be repaid in full or in part by proceeds from the EIDL loan.

If you would like International Accounting & Tax Consultants (IATC Inc) help with your accounting and tax issues please reach out to us at (202) 780-4494 or via email info@iatcpro.com.

by Donya Curry | Jan 5, 2020 | Bookkeeping

Here is a list of the Tax deadlines and dates you should be aware of for 2020.

January 15, 2020 4th Quarter 2019 Estimated Tax Payment Due

Self-employed fourth quarter estimated taxes are dues need to be paid by the January 15, 2020 tax deadline.

January 31, 2020 deadline for 2019 W-2s and 1099-MISC forms.

All 1099-MISC for contractors, and Form W-2’s to employees should be filed and given to them by this deadline. Penalties apply to businesses who fail to complete the deadline.

March 16, 2020 deadline for corporations, S-Corps, and LLCs returns (1120, 1120-S, 1065)

April 15, 2020 Deadline for personal tax returns. (1040)

Deadline for Trusts and Estate (1041). Foreign Bank Account Report Due (FinCen 114)

Last day to apply for an extension. (7004)

1st quarter estimated taxes due.

Last day to make your 2019 IRA Contribution

June 15, 2020 2nd Quarter 2020 Estimated Tax Payment Due

Self-employed second quarter estimated taxes are dues need to be paid by the January 15, 2020 tax deadline.

September 15, 2020 3rd Quarter 2020 Estimated Tax Payment Due

Self-employed third quarter estimated taxes are dues need to be paid by the January 15, 2020 tax deadline.

October 15, 2020 Extended Individual Tax Returns Due

If you got a filing extension on your 2019 tax return, you need to get it completed and postmarked by October 15, 2020.

January 15, 2021 4th Quarter 2020 Estimated Tax Payment Due

Self-employed fourth quarter estimated taxes are dues need to be paid by the January 15, 2020 tax deadline.

Recent Comments